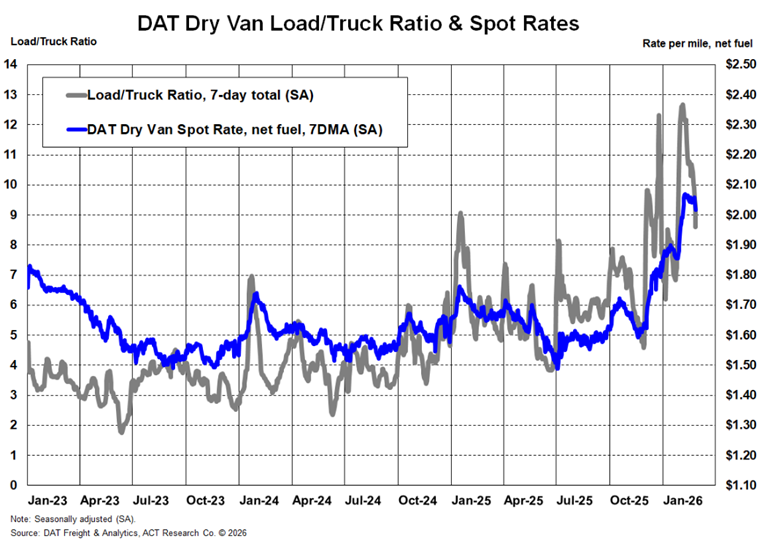

While not the only factor at work, severe weather has kicked the freight cycle into a new stage in recent months, with rates spiking as capacity was frozen, as discussed in the latest release of the Freight Forecast: Rate and Volume OUTLOOK report.

“Capacity contraction from low new equipment demand is also playing a part, so the reversion from weather should see rates fall to a new, higher floor. Aside from weather, freight demand conditions still aren’t wonderful, but received a modest boost from recent tariff changes,” shared Tim Denoyer, ACT Research’s Vice President and Senior Analyst.

“With retail inventories lean and a later Lunar New Year this year, we expect freight demand to improve after a soft March and April. But capacity contraction in terms of both equipment and drivers will be challenging to reverse.

“In seasonally adjusted terms, dry van truckload rates held up remarkably in February, ending the month above where they started, even as the market has opened back up. Downward reversion is nearly assured as weather warms, but the supply-driven tightening is currently pushing TL contract rates up in the mid-single-digit percentages for the first time in over four years,” Denoyer concluded.

Freight Forecast Report Overview

The monthly 58-page ACT freight forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast provides unmatched detail on the freight rate outlook, helping companies across the supply chain plan with greater visibility and less uncertainty.

ACT Research Overview

ACT Research is recognized as the leading publisher of commercial vehicle truck, trailer, and bus industry data, market analysis and forecasts for the North America and China markets. ACT’s analytical services are used by all major North American truck and trailer manufacturers and their suppliers, as well as banking and investment companies. ACT Research is a contributor to the Blue Chip Economic Indicators and a member of the Wall Street Journal Economic Forecast Panel. ACT Research executives have received peer recognition, including election to the Board of Directors of the National Association for Business Economics, appointment as Consulting Economist to the National Private Truck Council, and the Lawrence R. Klein Award for Blue Chip Economic Indicators’ Most Accurate Economic Forecast over a four-year period. ACT Research senior staff members have earned accolades including Chicago Federal Reserve Automotive Outlook Symposium Best Overall Forecast, Wall Street Journal Top Economic Outlook, and USA Today Top 10 Economic Forecasters. More information can be found at www.actresearch.net.

Additional Resources

Truckload spot rates spent three to four weeks up double-digit percentages y/y in late December and early January, and weather remains a near-term risk to truckload capacity, as discussed in the latest release of the Freight Forecast: Rate and Volume OUTLOOK report.

“Most of the jump in spot rates was due to severe weather, but Class 8 orders also rose in December with improved truckload conditions and a degree of clarity for EPA’27 low-NOx regulations. We expect a small equipment capacity contraction in 2026, but one that will likely continue in 2027.

“Growth has been led largely by a narrow segment of the economy, but it has room to broaden out if the looming Supreme Court tariff decision brings tariffs down,” said Tim Denoyer, ACT Research’s Vice President and Senior Analyst. “This would lead to additional broad disinflation, providing more leeway for the Fed to further lower rates, spurring freight-sensitive sectors like housing and durable goods. After destocking in Q4’25, we think the Supreme Court decision on IEEPA tariffs could provide a positive catalyst for freight demand.”

“On the other hand, upholding the tariffs would further extend the recessionary conditions the trucking industry has been contending with for the past four years, by pressing prices up further.

“The average age of a US Class 8 tractor is now 6.3 years old, the highest in more than a decade, which should help usher in a new phase of the truckload cycle,” Denoyer concluded.

Click here to learn more information about ACT's most subscribed report.

ACT Research is featured regularly by major news outlets for our work covering Class 8 truck orders, sales, forecasting, used truck sales, freight rates, trailer sales, and much more. Get more trends, HERE.