Commercial Vehicle & Freight Market Intelligence for Investors and Financiers

Connect freight, equipment, production, used value, and regulatory signals to stronger investment, credit, and capital planning decisions.

ACT Research helps investors, lenders, finance companies, and capital-market teams understand the freight and commercial vehicle signals shaping transportation-sector risk and opportunity. With forward-looking forecasts, market data, and analyst interpretation, ACT gives your team a clearer view of demand, production, used equipment values, freight conditions, powertrain change, and regulatory timing — so you can evaluate market exposure and build more defensible assumptions.

Get Transportation IntelligenceBuild investment and credit decisions around a clearer market view.

Transportation markets move in cycles, and those cycles create both risk and opportunity. Freight rates, carrier profitability, Class 8 demand, production trends, trailer activity, used truck values, powertrain adoption, and regulatory timing can all affect investment performance, credit exposure, collateral values, and capital allocation.

ACT helps investors and financiers connect these signals into a forward-looking market view that supports stronger modeling, underwriting, portfolio monitoring, and strategic decision-making.

- Market-Cycle Intelligence: Track the freight, equipment, production, and economic signals that shape transportation-sector performance.

- Asset & Collateral Context: Monitor used truck values, equipment demand, inventory, and replacement-cycle signals that may affect residual risk and collateral exposure.

- Forward-Looking Forecasts: Use commercial vehicle, freight, trailer, powertrain, and used equipment forecasts to support investment models and planning assumptions.

- Regulatory & Technology Outlook: Understand how emissions requirements, ZEV adoption, infrastructure readiness, and powertrain shifts may affect future demand and capital risk.

July 2026 Update

Investor Market Update“I would recommend ACT as your number 1 ‘go to’ source for industry forecasts and just general industry knowledge…You cannot follow this industry, be part of this industry without knowing what ACT Research is saying….”

Mike Zimm

BMO

Market intelligence for investment, credit, and capital-risk decisions

ACT Research helps investment and finance teams evaluate the market signals that influence transportation-sector performance, asset values, credit quality, and growth potential.

Our forecasts and market intelligence connect freight conditions, commercial vehicle demand, production trends, used equipment values, and powertrain adoption to the decisions investors and financiers need to make.

- Market Trends & Sector Health: Track demand cycles, order activity, production, backlog, inventory, and capital equipment indicators across Class 4–8 trucks and trailers.

- Freight & Economic Indicators: Evaluate freight volume, rate movement, and economic activity to assess demand potential, revenue pressure, and transportation-market health.

- Asset Value & Residual Risk Signals: Monitor used truck pricing, inventory, resale value, and equipment-cycle conditions that may affect collateral values and portfolio risk.

- Alternative Powertrain Forecasting: Assess battery-electric, hydrogen fuel cell, natural gas, and other powertrain trends tied to regulation, infrastructure, and adoption timing.

- Competitive & Market Structure Context: Understand OEM dynamics, segment divergence, M&A considerations, and broader commercial vehicle ecosystem trends.

Who uses ACT investor intelligence?

ACT supports capital-market and finance teams that need a clearer view of transportation market cycles, asset risk, and future demand.

- Capital Finance Companies: Evaluate demand cycles, equipment values, production trends, and collateral risk to support financing decisions.

- Lenders and Credit Teams: Monitor freight conditions, carrier health, used equipment values, and segment-level risk for stronger underwriting and portfolio management.

- Private Equity and Venture Capital Firms: Identify market-cycle opportunities, technology adoption trends, and commercial vehicle segments with changing growth potential.

- Portfolio Managers and Financial Analysts: Use freight, production, and equipment-market signals to inform models, allocations, and company-level analysis.

- Sustainability-Focused Funds: Track zero-emission vehicle adoption, infrastructure readiness, and regulation-driven demand shifts.

- Hedge Funds and Institutional Investors: Evaluate industry cycles, demand signals, freight fundamentals, and production trends that may affect market expectations.

Three strengths behind ACT market intelligence

ACT combines proprietary market data, disciplined forecasting methodology, and experienced analyst interpretation to help customers understand not only what changed in the market, but what those signals may mean for future planning decisions.

ACT Methodology

ACT’s forecasting methodology is built on decades of market-cycle experience, industry relationships, historical data, and disciplined analysis.

We connect freight demand, equipment supply, economic activity, production trends, used equipment values, regulatory factors, and customer behavior to help customers evaluate the market with a balanced, forward-looking view.

ACT Proprietary Data

ACT’s market view begins with direct visibility into the freight, equipment, and commercial vehicle signals that shape transportation planning decisions.

By tracking market indicators across commercial vehicles, freight, trailers, used equipment, and broader economic activity, ACT helps customers understand what is changing, how signals connect, and what those shifts may mean for the road ahead.

ACT Human Intelligence

ACT’s analysts bring deep experience across freight, equipment, commercial vehicle, used truck, trailer, regulatory, and economic markets.

We do not simply report the data. We interpret what market signals may mean, how they connect across the transportation cycle, and what decisions they may help inform.

Forecasts and market intelligence investors rely on

North America Commercial Vehicle Outlook

Commercial vehicle forecasts for demand, production, and market planning.

ACT’s North America Commercial Vehicle Outlook helps manufacturers evaluate demand trends across Classes 4–8 vehicles and trailers over near- and long-term planning horizons.

It connects vehicle demand, economic indicators, fleet population trends, and market-cycle movement to help manufacturers align production, capacity, and strategic planning with future market conditions.

What It Offers

- Class 4–8 vehicle and trailer forecasts across 1-, 5-, and 10-year horizons

- Economic and industry drivers shaping commercial vehicle demand

- Fleet population, age, and replacement-cycle insights

- Market context for production, capacity, and demand planning

Who Benefits

- OEMs and suppliers aligning production and capacity with market demand

- Strategy, finance, and sales teams building market assumptions

- Investment and research teams tracking commercial vehicle industry performance

North America Commercial Vehicle Outlook Plus

Commercial vehicle demand, powertrain, and regulatory intelligence for long-term planning.

ACT’s North America Commercial Vehicle Outlook Plus provides a forward-looking view of commercial vehicle demand, zero-emission vehicle adoption, powertrain trends, infrastructure readiness, and regulatory timing.

It helps manufacturers and suppliers evaluate how emissions requirements, technology adoption, and customer behavior may affect production planning, product strategy, and long-term investment.

What It Offers

- North America Commercial Vehicle Outlook coverage and monthly market updates

- Bottom-up forecasts for battery-electric, hydrogen fuel cell, and natural gas vehicles across Classes 4–8

- Infrastructure readiness analysis for charging and hydrogen refueling

- U.S. and Canadian emissions regulation timelines and planning implications

Who Benefits

- OEMs and Tier 1 suppliers planning product, production, and powertrain strategy

- Engine, component, and infrastructure suppliers evaluating future demand

- Fleet and finance teams assessing technology timing and total cost implications

U.S. Used Truck Price Forecast

Used truck value intelligence for collateral, residual-risk, and market-cycle analysis.

Used truck values can provide an important signal for transportation-sector health, fleet behavior, replacement timing, and collateral exposure.

ACT’s U.S. Used Truck Price Forecast helps investors, lenders, finance companies, and analysts evaluate used Class 8 tractor price trends by age and mileage group, with market context tied to freight demand, new truck availability, inventory, and macroeconomic conditions.

What It Offers

- Monthly used truck price forecasts for Class 8 tractors by age and mileage group

- Economic and market drivers affecting used truck prices

- Inventory, resale value, and replacement-cycle context

- Market intelligence for residual-risk and collateral-value analysis

Who Benefits

- Lenders and finance companies assessing collateral values and residual risk

- Investors and analysts using used truck prices as a transportation-sector health indicator

- Dealers, fleets, and remarketing teams evaluating inventory and resale expectations

Freight & Transportation Forecast

Rate, volume, and freight-cycle intelligence for manufacturing demand context.

Freight conditions influence fleet profitability, replacement timing, equipment demand, and customer urgency. ACT’s Freight & Transportation Forecast helps manufacturers connect freight market movement to broader equipment and commercial vehicle demand.

What It Offers

- Truckload contract and spot rate forecasts for dry van, refrigerated, and flatbed markets

- Cass Shipments and Truckload Linehaul Index forecasts

- ACT Freight Composite Index Forecast, a freight-weighted measure of economic activity

- LTL and intermodal rate and volume forecasts

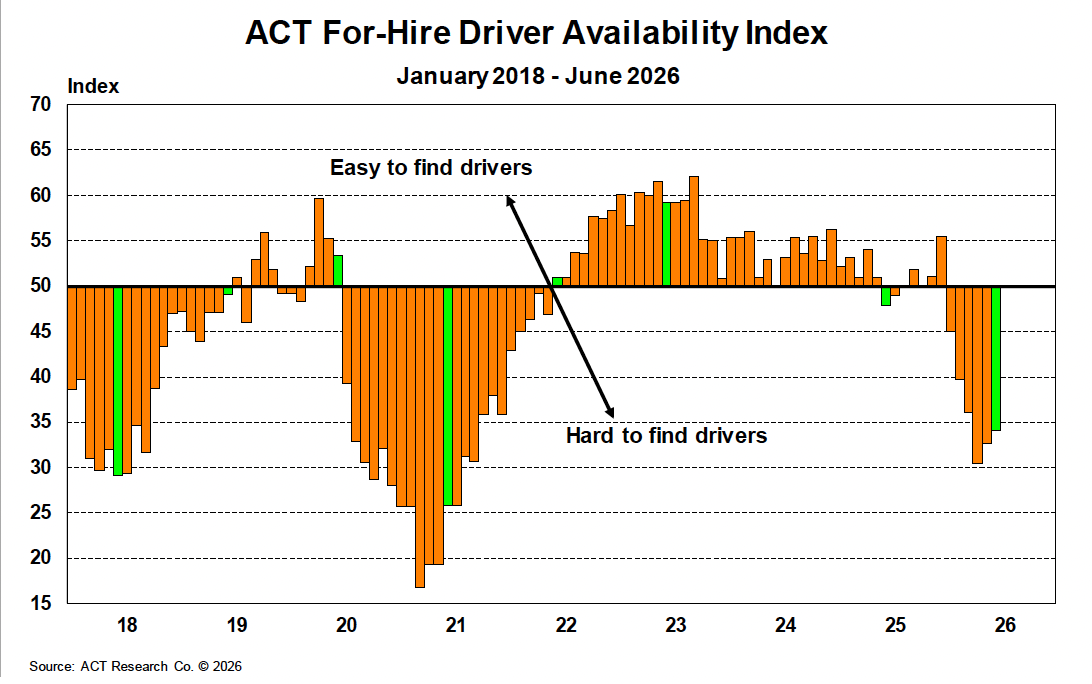

- ACT For-Hire Survey Indexes covering rates, drivers, equipment, and fleet sentiment

Who Benefits

- OEMs and suppliers connecting freight conditions to future equipment demand

- Fleet and finance teams evaluating freight-cycle timing

- Strategy and market intelligence teams assessing transportation market health

North America Classes 5-8 Vehicles

Comprehensive Market Intelligence on North American Class 5-8 Vehicles

What It Offers:

- Monthly Production and Sales Data: In-depth coverage of monthly production, sales, and inventory levels for Class 5-8 trucks, providing critical insights into current and projected market conditions.

- Order Backlogs and Cancellation Rates: Detailed analysis of order backlogs, cancellation rates, and their implications for future demand, supporting accurate assessments of market momentum.

- Insights on Supply Constraints: Up-to-date information on supply chain pressures affecting Class 5-8 production, from parts shortages to labor availability, helping stakeholders manage and anticipate impacts on production timelines.

Who Benefits?

- OEMs and Tier 1 Suppliers optimizing production planning and adjusting to supply chain conditions based on total market data.

- Fleet Owners and Equipment Managers evaluating market trends to make informed decisions on fleet expansion, replacement, and capital investments.

- Logistics Companies and Freight Brokers monitoring equipment availability and market demand to plan capacity needs effectively.

- Investors and Analysts seeking data-driven insights into the performance and trajectory of the Class 5-8 market to guide investment strategies.

NA OEM Classes 5-8 Build & Retail Sales

Detailed Build and Retail Sales Data for North American Commercial Vehicles

What It Offers:

- Production and Retail Sales Tracking: Monthly updates on build rates and retail sales figures for Class 5-8 commercial vehicles, providing a clear snapshot of the market’s production output and sales performance.

- Market Comparisons Across Classes: Comparative analysis across Class 5-8 vehicle segments, offering nuanced insights into performance differences and trends within each vehicle class.

Who Benefits?

- OEMs and Suppliers optimizing production and inventory planning based on accurate build and retail data.

- Dealers and Distributors assessing market demand to align inventory with retail trends and improve stock management.

- Fleet Operators and Procurement Teams using production and sales insights to time acquisitions and optimize fleet investments.

- Investors and Analysts tracking sales and production data as leading indicators of the commercial vehicle market's health and growth potential.

Updated July 31, 2026

Market Update - Investors & Financiers

July 2026 Update

Supply Tightening Strengthens the Investment Signal as Pricing Power Accelerates

July data point to a transportation market moving further into a supply-driven upturn. Freight demand remains uneven, but acute truckload capacity tightness, sharply higher spot rates, and accelerating contract pricing are strengthening the market-cycle signal for investors and financiers. ACT’s latest Freight Forecast shows aggregate spot rates, excluding fuel, increased 43% year over year in June, while contract rates were 13% higher.

For investors, lenders, equipment finance teams, and credit analysts, the current environment is increasingly about pricing power, capacity discipline, collateral performance, and margin durability—not broad volume growth. Driver scarcity, continued capacity contraction, regulatory enforcement, and limited fleet expansion are supporting higher rate floors, although elevated operating costs continue to limit the earnings benefit for some carriers.

Key Takeaways for Investors

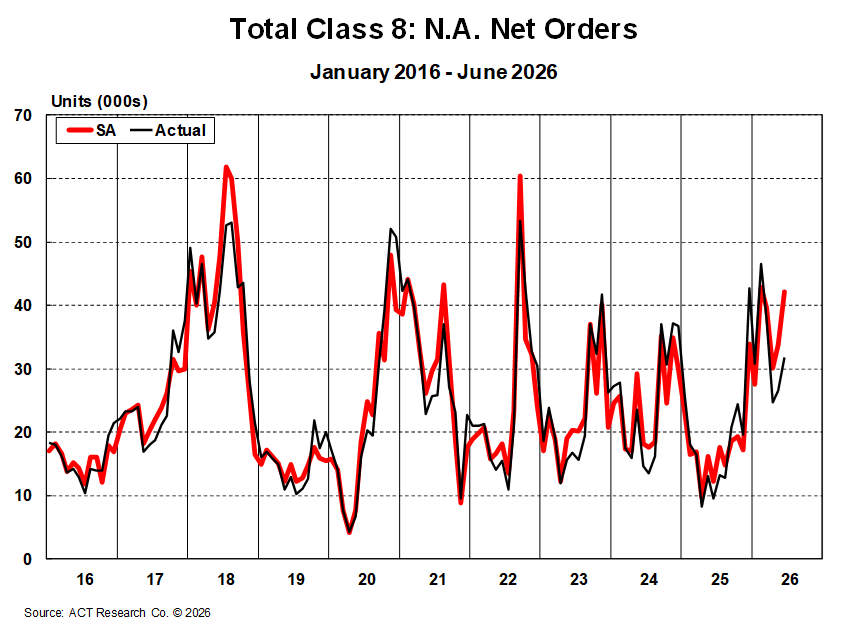

- Class 8 Orders Strengthen, but Expansion Remains Disciplined

North American Class 8 orders strengthened further in June, more than tripling year over year and increasing 25% sequentially on a seasonally adjusted basis. Tractor demand led the improvement as tighter capacity, stronger freight rates, replacement needs, and EPA 2027 planning supported fleet interest.

Class 8 backlogs reached a 38-month high, improving production visibility for OEMs and suppliers. Third- and fourth-quarter build plans also moved higher. From a financial perspective, these signals are constructive, but they do not necessarily indicate broad fleet expansion.

Elevated equipment prices, financing costs, insurance expenses, and uneven carrier profitability continue to reinforce disciplined purchasing. Investors and lenders should monitor order quality, cancellations, backlog conversion, replacement timing, and whether higher freight rates translate into sufficient cash flow to support equipment commitments.

- Freight Volumes Remain Uneven as Rate Floors Move Higher

Freight demand is improving selectively, and some freight is shifting from private fleets back toward the for-hire market. However, the current rate upturn is still being driven primarily by constrained supply rather than a broad shipment surge.

This distinction matters for earnings expectations, credit quality, and asset-performance assumptions. Spot rates are leading the cycle, contract rates are following, and carrier pricing power has improved. However, insurance, labor, maintenance, equipment, and financing costs continue to absorb part of the revenue benefit.

For credit and investment teams, margin durability may depend more on yield discipline, network quality, customer mix, equipment utilization, and cost control than on volume acceleration. Companies that add capacity or costs before demand strengthens could remain vulnerable even in a higher-rate environment.

- EPA 2027 Supports Planning, but Prebuy Timing Remains Uncertain

EPA 2027 remains an important variable for Class 8 demand, capital spending, and equipment financing. Fleets are evaluating replacement exposure, equipment availability, and potential changes in acquisition and operating costs.

For investors and financiers, the question is not simply whether a prebuy develops, but how large, concentrated, and financeable it becomes. A meaningful pull-forward could strengthen OEM and supplier revenue visibility, increase equipment finance demand, and affect production schedules and residual-value assumptions.

The timing remains uncertain. Elevated borrowing costs, high equipment prices, insurance pressure, and uneven fleet profitability may keep purchasing measured. Financial teams should monitor orderboard activity, build-slot demand, regulatory developments, financing applications, and whether orders convert into completed deliveries.

- Pricing Power Is Improving, but Margin Quality Remains Selective

Aggregate truckload spot rates remained above contract rates in June, while contract pricing increased 13% year over year. That combination indicates that pricing strength is extending beyond short-term disruption and into broader shipper-carrier negotiations.

The margin implications will vary across carriers. Operators with stronger networks, disciplined customer selection, reliable equipment, and manageable insurance and financing exposure may capture more of the rate improvement. Less efficient or highly leveraged fleets could continue experiencing pressure despite higher revenue per mile.

Used truck values and transaction activity also remain important indicators for asset-backed lenders, lessors, dealers, and investors with residual-value exposure. Firmer freight rates may improve replacement confidence and used-equipment demand, but collateral performance remains sensitive to fleet profitability, financing availability, equipment condition, and the pace of new-truck deliveries.

Financial teams should continue monitoring:

· Spot- and contract-rate durability

· Carrier margin conversion and free cash flow

· Driver availability and for-hire capacity

· Used truck values, transaction activity, and residual risk

· Class 8 order quality, cancellations, and backlog conversion

· Trailer backlog rebuilding and segment-level demand

· EPA 2027 timing, financing needs, and regulatory developments

Bottom Line: A Supply-Driven Upturn Gains Traction

July reporting supports the view that the transportation and commercial vehicle cycle is moving further away from the excess-capacity conditions that defined the prior downturn. Freight demand is not broadly accelerating, but capacity is tighter, spot rates are sharply higher, contract pricing is responding, and Class 8 demand is improving from trough conditions.

For investors and financiers, the central signal remains a supply-driven upturn rather than a demand-led expansion. That distinction should shape earnings expectations, credit underwriting, residual-value assumptions, equipment finance planning, and portfolio monitoring.

Companies with stronger cost control, balance-sheet flexibility, replacement-driven equipment exposure, and disciplined capacity management may be better positioned. However, investors should continue distinguishing between revenue improvement and durable margin recovery, particularly where insurance, labor, maintenance, equipment, and financing costs remain elevated.

This is not investment advice. These market signals provide context for research, underwriting, due diligence, portfolio monitoring, and strategic planning as freight, equipment, and credit conditions evolve.

Why investors and financiers choose ACT Research

Investment and credit decisions require more than a single market signal. ACT combines direct market data, disciplined forecasting methodology, analyst expertise, and long-standing industry relationships to help investors and financiers understand the freight and commercial vehicle signals shaping risk, opportunity, and market performance.

- Proprietary commercial vehicle, freight, and used equipment market data

- Forecast methodology built on decades of market-cycle experience

- Analyst interpretation that connects demand, production, freight, and asset-value signals

- Market intelligence used by transportation, manufacturing, finance, leasing, and investment teams

- Trusted perspective for evaluating industry cycles, credit exposure, and capital-market risk

Market guidance for investment and credit decisions

ACT helps investors and finance teams understand the market signals that affect transportation-sector performance, asset values, credit quality, and capital allocation.

Our intelligence supports teams responsible for investment research, underwriting, portfolio monitoring, asset valuation, risk management, and executive planning with a clearer view of freight conditions, equipment demand, production trends, used truck values, powertrain adoption, and regulatory timing.

With ACT Research, investment and finance teams can:

- Make stronger strategic decisions with current market analysis and forward-looking commercial vehicle and freight forecasts.

- Evaluate credit and collateral exposure with better visibility into used truck values, equipment demand, freight conditions, and carrier health.

- Connect freight conditions to equipment demand by understanding how rates, fleet profitability, and replacement cycles may affect commercial vehicle markets.

- Assess regulatory and powertrain risk with intelligence on emissions timing, ZEV adoption, engine demand, and infrastructure readiness.

- Spot risks and opportunities earlier across freight, economic, regulatory, equipment, and powertrain-cycle signals.

- Support models and investment theses with market assumptions your team can defend.

Ready to connect market signals to your next investment or credit decision?

ACT helps investors and financiers connect freight conditions, commercial vehicle demand, production trends, used equipment values, powertrain change, and regulatory timing to stronger market analysis and capital planning decisions.

Whether your team is evaluating credit exposure, monitoring portfolio risk, building an investment thesis, assessing collateral values, or tracking transportation-sector cycles, ACT can help you develop a clearer view of what comes next.

Questions about the right intelligence for your investment or credit decisions?

ACT can help you identify the forecasts, market data, and analyst perspective that fit your research, underwriting, portfolio, or capital-planning needs.