Freight Trucking Rates

Truck Freight Rates: March 2026 Van, Reefer & Flatbed Update

ACT Research provides consolidated, forward-looking freight rate analysis — helping carriers, brokers, and shippers plan contract strategy with confidence.

Freight & Trucking Rate Update

March 27, 2026

As of March 2026, the freight and trucking industry is entering the year with firmer momentum than previously expected, driven less by weather-related disruption and increasingly by structural capacity tightening. While underlying goods demand remains mixed and inventory behavior cautious, accelerating capacity contraction, declining driver availability, and rising fuel costs have meaningfully tightened the market entering late Q1. Recent disruptions tied to winter weather have largely passed, but their impact revealed a materially leaner supply environment that continues to support elevated rate conditions.

Unlike prior periods in 2024–2025, current spot rate strength reflects both structural capacity constraints and cost-driven pressures. Spot truckload rates, net fuel, are running roughly 20% higher year-over-year into March, with load postings still elevated and capacity availability constrained across key regions. While some seasonal moderation is expected as backlogs clear and conditions normalize, higher diesel prices are simultaneously tightening supply and reinforcing elevated rate floors.

Below are the latest insights on dry van, flatbed, and reefer rates based on ACT Research’s March 2026 Freight Forecast.

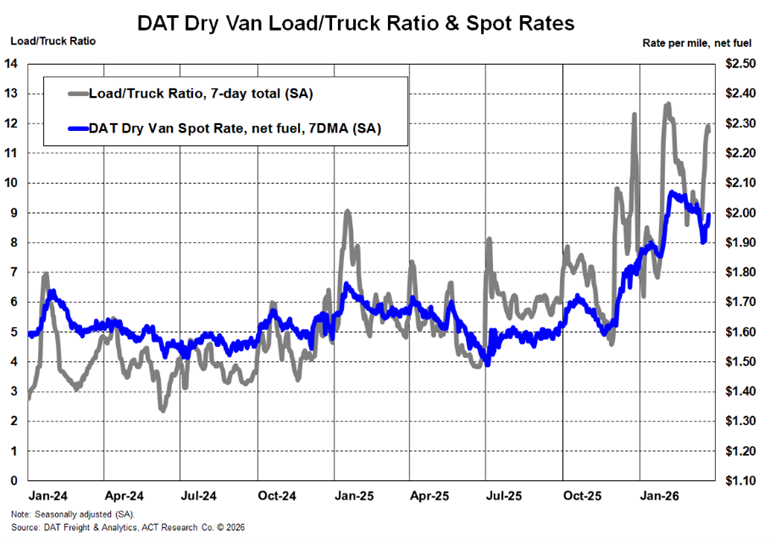

Dry Van

Dry van spot rates remained elevated into March following the winter-driven surge, supported by structurally tighter capacity and rising operating costs. While load postings have moderated from peak weather-driven levels, they remain significantly higher year-over-year, indicating sustained demand relative to available capacity. Spot rates continue to reflect roughly 20% year-over-year gains, though near-term pressure from higher diesel costs may create some volatility in net pricing.

ACT continues to expect some seasonal normalization as conditions stabilize, but with capacity still constrained and private fleet contraction supporting for-hire demand, dry van rates are likely to hold at higher floors compared to 2024–2025. Sustained upside will depend on broader demand recovery through the spring and summer months.

Flatbed

Flatbed spot rates have shown modest improvement but continue to lag other segments in overall momentum. Industrial freight remains uneven, though rising energy sector activity tied to higher oil prices is providing incremental support. Infrastructure investment and data-center buildouts continue to offer stability, but broader construction and manufacturing softness remains a limiting factor.

Capacity conditions in flatbed are tightening gradually, though not yet to levels that would drive sustained pricing power. Near-term rate direction will remain closely tied to energy markets and the pace of industrial recovery.

Reefer

Reefer spot rates remain the strongest-performing segment, with year-over-year gains still well above dry van levels. Tight specialized capacity, combined with earlier weather disruptions and ongoing supply constraints, has supported elevated pricing into March.

While some normalization is expected as seasonal patterns stabilize, the underlying capacity environment remains tight. As a result, reefer rates are expected to maintain stronger relative performance, with full-year expectations remaining above prior forecasts.

Contract Rates

Dry Van

Dry van contract rates are accelerating more clearly as sustained spot market strength and higher fuel costs move through bid cycles. Fuel surcharges are contributing to upward pressure, and carrier leverage is improving modestly as capacity tightens. While increases remain measured, the pricing environment has shifted in favor of carriers for the first time in several years.

Flatbed

Flatbed contract rates remain relatively stable, reflecting continued softness in industrial demand. While spot stabilization is constructive, meaningful contract rate acceleration will likely require broader improvement across construction and manufacturing sectors.

Reefer

Reefer contract rates continue to firm gradually, supported by sustained spot strength and tightening capacity. Carriers are beginning to regain negotiating leverage, though the pace of increase remains dependent on the durability of current spot rate levels.

Summary

Entering March 2026, the freight market is firmer than at any point in the past several years, with recent gains increasingly supported by structural capacity constraints rather than temporary disruptions. Spot rates remain elevated on a year-over-year basis, while contract rates are beginning to accelerate, signaling a broader shift in pricing dynamics.

Carriers continue to navigate elevated input costs, including a sharp rise in diesel prices, alongside tariff-driven equipment inflation and regulatory-driven driver supply constraints. Many fleets remain disciplined in capital deployment, focusing on replacement timing and operational efficiency rather than expansion.

While some near-term volatility is expected as seasonal factors normalize and fuel costs fluctuate, the structural setup has improved meaningfully. Continued capacity tightening, regulatory pressures, and gradually improving demand conditions support a more constructive outlook for the remainder of 2026, with a more durable recovery increasingly driven by sustained rate strength rather than short-term dislocations.

To see how freight trucking rates change in the future, and for detailed analysis and forecasts, see ACT's freight & transportation forecast.

While contract rates are accelerating and spot rates remain materially higher year-over-year despite expected seasonal normalization, the strong rebound in Class 8 orders has not yet translated into broad-based expansion. Backlogs have improved and inventories are healthier, but carrier profitability remains uneven as rising fuel and operating costs offset rate gains. With tariff-driven equipment inflation and higher diesel prices pressuring total cost of ownership, fleets remain disciplined, and the recovery continues to be driven more by structural capacity tightening and constrained driver supply than by a demand-led surge, keeping most strategies focused on replacement timing, regulatory positioning, and cost control rather than expansion.

Tim Denoyer

VP & Sr. Analyst

Resources

Whether you’re new to our company or are already a subscriber, we encourage you to take advantage of all our resources.