Freight Trucking Rates

Truck Freight Rates: June 2026 Van, Reefer & Flatbed Update

ACT Research provides consolidated, forward-looking freight rate analysis — helping carriers, brokers, and shippers plan contract strategy with confidence.

Freight & Trucking Rate

June 2026 Update

June 26, 2026

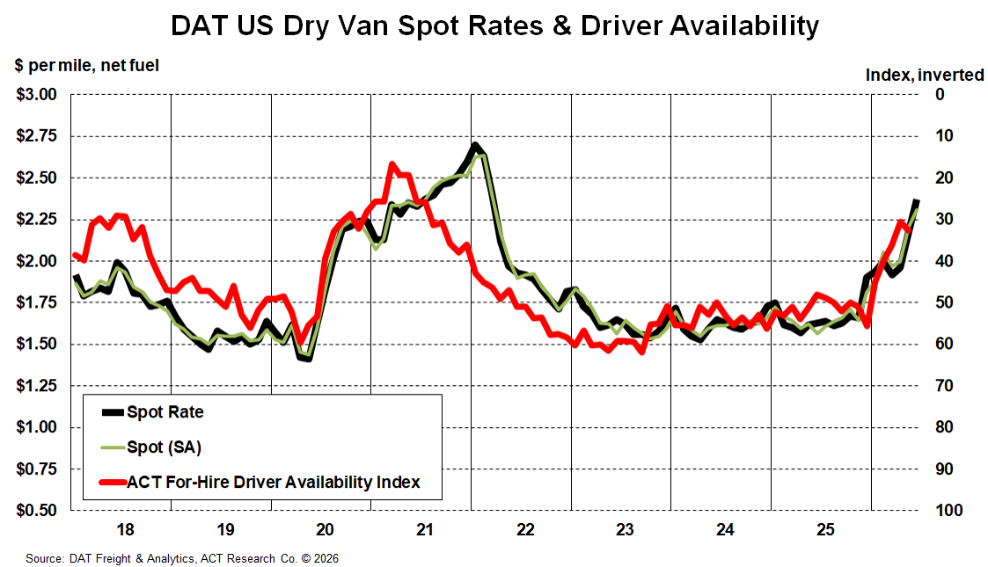

As of June 2026, the freight and trucking rate environment has tightened quickly, with pricing strength now extending beyond short-term spot volatility. The main driver remains supply-side pressure: driver availability has fallen sharply, capacity has contracted, and regulatory/enforcement changes are tightening the market faster than freight demand alone would suggest. ACT’s June Freight Forecast notes that the market has entered a period of rising rates and tight capacity.

Spot truckload rates are now meaningfully higher year-over-year across dry van, flatbed, and reefer, with flatbed reaching a new record high in May. Contract rates are also accelerating, confirming that the pricing reset is moving into bid activity and broader carrier revenue quality. Aggregate DAT contract rates rose again in May and were nearly 10% above year-ago levels.

Below are the latest insights on dry van, flatbed, and reefer rates based on ACT Research’s June 2026 Freight Forecast.

Dry Van

Dry van rates continue to reflect a truckload market that has moved firmly into recovery. Spot rates accelerated again in May, supported by tighter available capacity, Roadcheck-related pressure, and stronger load activity moving into the spot market.

Capacity remains the key story. Demand is improving, but the larger rate driver is the reduction in available trucks and drivers. Shippers should expect less pricing relief than during the prior downcycle, while carriers are regaining leverage as spot strength begins to influence contract discussions.

Flatbed

Flatbed is currently one of the strongest truckload segments. ACT’s June Freight Forecast shows flatbed spot rates rose sharply in May to a record high, up more than 30% year-over-year, with June starting well ahead of normal seasonal patterns.

The segment is benefiting from construction season, energy activity, data-center-related power generation demand, and tighter specialized capacity. Flatbed contract rates are also moving higher, reflecting that the improvement is no longer limited to short-term spot conditions.

Reefer

Reefer rates remain elevated and capacity-sensitive. ACT’s June Freight Forecast shows reefer contract rates increased again in May and were up year-over-year, with ACT expecting stronger gains in 2026 and 2027 given capacity risk in the reefer market.

The reefer market remains vulnerable to seasonal volatility, especially around produce demand and temperature-controlled freight cycles. If specialized capacity remains tight, spot strength should continue to pressure contract pricing.

Contract Rates

Contract rates are now responding more clearly to sustained spot-market strength. Aggregate DAT contract rates, combining dry van, reefer, and flatbed, rose in May and were up 9.8% year-over-year. ACT expects the recent spot-rate acceleration to drive a more meaningful contract-rate increase in the second half of 2026.

For shippers, the contract market is becoming less favorable than it was during the 2024–2025 downturn. For carriers, improving contract rates should support revenue quality, though insurance, labor, equipment, financing, and other operating costs continue to pressure margins.

Summary

Entering June 2026, freight rates are strengthening as the market shifts further into a supply-driven recovery. Dry van conditions are firmer, flatbed has moved to the front of the rate cycle, and reefer remains capacity-sensitive with upside risk during seasonal peaks.

The recovery remains uneven, but the pricing direction is clearer than earlier in the year. Shippers, carriers, brokers, fleets, and investors should continue monitoring spot-contract spreads, driver availability, regulatory enforcement, seasonal demand, and whether improving rates translate into healthier carrier profitability.

To see how freight trucking rates change in the future, and for detailed analysis and forecasts, see ACT's freight & transportation forecast.

While contract rates are accelerating and spot rates remain materially higher year-over-year, the June reports reinforce that the recovery is still being driven more by constrained supply than by a demand-led surge. Driver availability has fallen sharply, regulatory and enforcement pressure is tightening capacity, and Roadcheck confirmed a market that has shifted back toward carrier leverage. Class 8 order activity has improved meaningfully from depressed levels, led by stronger tractor demand, but it still reflects disciplined replacement and regulatory positioning more than broad-based fleet expansion.

Backlogs are improving and production visibility is better, while carrier profitability remains uneven as insurance, financing, equipment, labor, and other operating costs offset some of the benefit from higher rates. With EPA 2027 timing approaching and total cost of ownership still elevated, fleets remain selective. Most strategies continue to center on replacement timing, capacity planning, regulatory positioning, and cost control rather than aggressive growth.

Tim Denoyer

VP & Sr. Analyst

Resources

Whether you’re new to our company or are already a subscriber, we encourage you to take advantage of all our resources.