Class 8 Truck Orders

June 2026 Class 8 Truck Orders & Industry Outlook

ACT Research delivers proprietary, forward-looking analysis of Class 8 truck orders to help industry leaders plan capacity and capital investments with confidence.

Class 8 Truck Orders

June 2026 Update

June 26, 2026

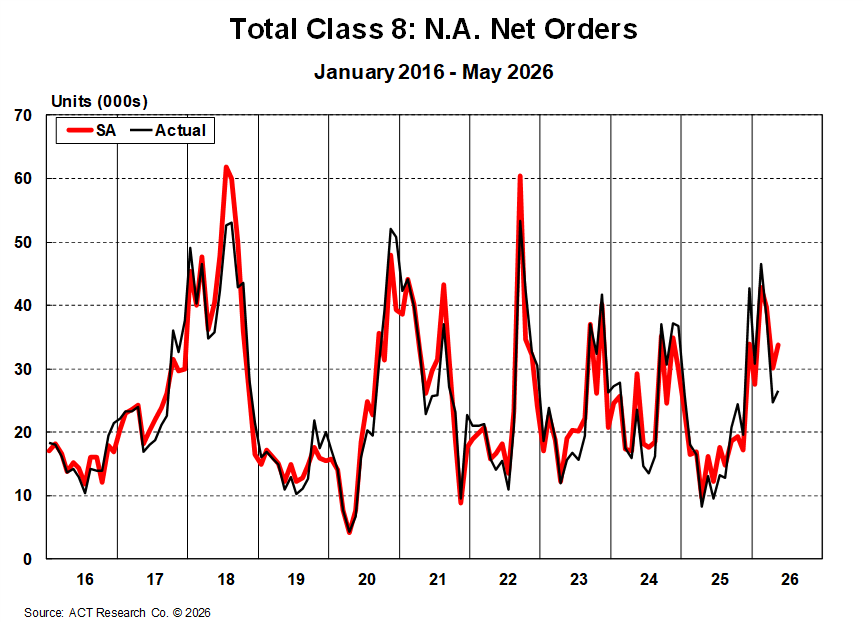

Class 8 order activity strengthened in May, reinforcing that the market is moving further off the bottom. North American Class 8 orders rose sharply year-over-year and improved sequentially on a seasonally adjusted basis, with tractor demand leading the gain. Stronger spot and contract rates, tighter capacity, lower driver availability, and EPA 2027 timing are all supporting renewed demand.

Backlog and production signals remain constructive. Class 8 backlogs increased to a multi-year high, giving OEMs better production visibility, while build plans moved higher for the back half of 2026. Retail sales remain a more cautious signal, suggesting fleet capital deployment is improving but still disciplined and closely tied to profitability, financing conditions, and confidence in the freight-rate recovery.

Class 8 Truck Orders Snapshot

June’s Class 8 truck orders update points to a recovery that is gaining traction, but still being driven more by supply-side tightening than broad freight demand growth. The strongest support is coming from constrained capacity, rising freight rates, regulatory pressure, replacement demand, and pre-EPA 2027 planning.

OEMs continue to benefit from stronger backlog visibility, while fleets remain selective around timing, total cost of ownership, and expected rate improvement. Dealers, suppliers, lenders, and investors should continue watching backlog quality, cancellation activity, retail sales, and whether higher freight rates translate into healthier carrier profitability.

The setup is more constructive than earlier in the cycle. If capacity remains constrained and freight rates continue to firm, Class 8 order activity should remain supported through the second half of 2026 and into 2027.

With May order activity strengthening sharply year-over-year and improving sequentially on a seasonally adjusted basis, Class 8 truck orders now point to a supply-driven recovery that is gaining traction, though not yet a broad-based demand surge. Orderboards are rebuilding from depressed levels, while OEMs continue to manage production carefully and stronger backlogs provide improved visibility. The market’s challenge has shifted from weak demand and backlog erosion toward tighter capacity, improving freight rates, and still-fragile carrier profitability. Regulatory clarity around 2027 equipment timing continues to support planning, while driver-related policy changes, FMCSA enforcement, and other capacity constraints are tightening supply. Elevated insurance, financing, equipment, and operating costs remain pressure points for total cost of ownership. Vocational demand remains resilient, supported by infrastructure, utility, grid, data-center, and AI-related investment, while tractor demand is benefiting from stronger truckload rate conditions. Retail activity is improving but still measured, leaving fleets focused on disciplined replacement, profitability, and regulatory positioning rather than broad-based expansion.

Kenny Vieth

President & Senior Analyst

Resources

Whether you’re new to our company or already a subscriber, we encourage you to take advantage of all our resources.