Trucking Industry 2027 Outlook

July 2026

Updated July 31, 2026

Trucking Industry Forecast 2027: Tighter Capacity Creates a Firmer Planning Environment

The Trucking Industry Forecast 2027 is increasingly being shaped by the supply constraints developing in 2026. Freight demand remains uneven, but contracting capacity, limited driver availability, sharply higher spot rates, and accelerating contract pricing are creating a firmer foundation for 2027 planning.

ACT’s July Freight Forecast shows aggregate truckload spot rates, excluding fuel, increased 43% year over year in June, while aggregate contract rates were 13% higher. The movement in contract pricing indicates that tighter market conditions are extending beyond short-term spot-market disruption and into shipper bids, transportation budgets, and contract renewals.

For fleets, carriers, brokers, shippers, dealers, leasing companies, lenders, manufacturers, suppliers, and investors, 2027 planning is likely to center on three questions: how durable the rate upturn becomes, how quickly the industry can respond to constrained capacity, and how regulatory developments affect replacement decisions.

EPA 2027 remains an important planning consideration, but fleet decisions will also be shaped by carrier profitability, financing costs, insurance expenses, used-truck values, equipment availability, and confidence that higher rates will produce sustainable cash-flow improvement.

Freight, Capacity, and Market Balance

The freight market forecast for 2027 is being influenced by a supply-driven upturn already taking shape in 2026. Freight activity is improving selectively, and some freight is shifting from private fleets back toward the for-hire market. However, the market is still not being driven by a broad shipment surge.

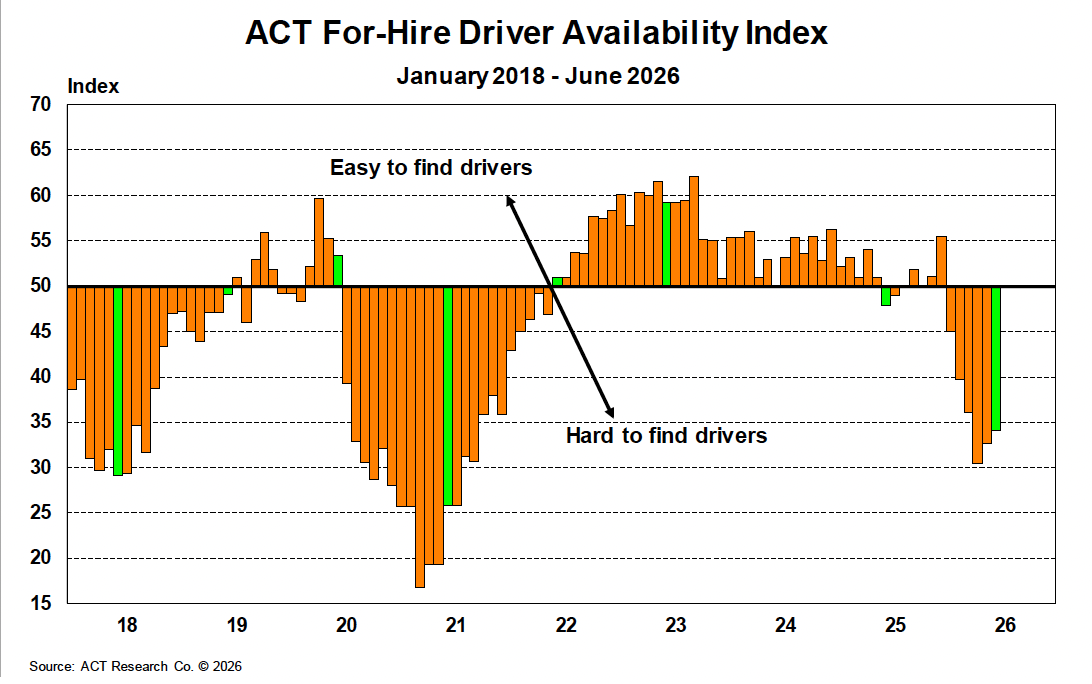

Capacity remains the central market signal. Driver availability is exceptionally tight, for-hire capacity continues to contract, and limited fleet investment is restricting the industry’s ability to respond quickly to higher rates. Compliance enforcement, driver-qualification requirements, and the removal of marginal capacity are also contributing to a less flexible supply base.

Spot rates continue to lead the market. Aggregate spot rates, excluding fuel, were 43% above year-ago levels in June and remained above contract rates. Aggregate contract rates increased seven cents during the month to $2.41 per mile and were 13% higher year over year.

For 2027, these conditions could support firmer freight-rate floors, improve carrier pricing power, and change procurement timing for shippers and brokers. However, higher revenue does not automatically create durable margin improvement. Insurance, labor, maintenance, equipment, and financing costs continue to absorb part of the rate benefit.

The market is not yet demand-led, but it has moved further away from the excess-capacity conditions that defined the prior downcycle. Some seasonal rate moderation remains possible, but market participants should not assume that softer freight periods will restore the capacity availability or purchasing leverage present earlier in the cycle.

Equipment Markets and Fleet Behavior

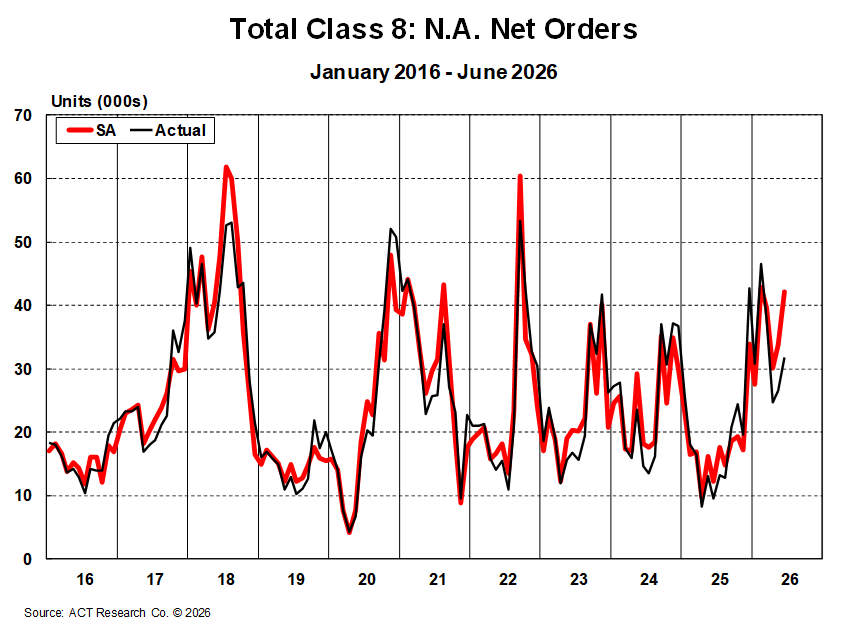

Equipment planning for 2027 is becoming more active as fleets evaluate replacement needs, equipment availability, freight-market profitability, and regulatory timing. North American Class 8 orders more than tripled year over year in June and increased 25% sequentially on a seasonally adjusted basis, with tractor demand leading the improvement.

Class 8 backlogs reached a 38-month high, improving production visibility for OEMs and suppliers. Third- and fourth-quarter 2026 build plans also moved higher, providing a firmer near-term production outlook.

Fleet behavior nevertheless remains disciplined. Replacement demand, financing conditions, equipment prices, operating costs, and confidence in the durability of higher freight rates are likely to shape purchase decisions more than broad capacity expansion.

Used-truck values and transaction activity are also becoming more relevant to 2027 planning. Firmer freight economics may support replacement confidence and trade activity, but used-equipment performance remains sensitive to fleet profitability, financing availability, equipment condition, and the pace of new-truck deliveries.

For commercial vehicle stakeholders, the 2027 truck market should be evaluated through replacement timing, order conversion, cancellations, used-equipment values, financing conditions, carrier cash flow, and the sustainability of freight-rate improvement.

Class 8

The Class 8 truck forecast for 2027 is supported by stronger freight economics, constrained capacity, replacement needs, and regulatory planning. Current signals suggest the market has moved beyond its weakest point, with better fleet sentiment and stronger production visibility than earlier in the cycle.

The central question is whether higher freight rates translate into sustained profitability and purchasing power. Fleets may have a stronger economic case for replacing aging tractors, but elevated equipment costs, insurance expenses, and financing sensitivity could continue to limit expansion-oriented buying.

EPA 2027 adds another timing consideration. Fleets are evaluating potential acquisition and operating-cost changes, equipment availability, and whether replacement purchases should be accelerated. The eventual size and timing of any prebuy remain uncertain because fleet balance sheets and financing capacity vary considerably.

For fleets, dealers, lenders, manufacturers, and suppliers, the most important 2027 Class 8 indicators include:

- Order quality and order-to-delivery conversion

- Backlog coverage and cancellation activity

- Replacement demand versus fleet expansion

- Carrier profitability and cash-flow improvement

- Used-truck values and trade activity

- Equipment pricing and financing availability

- EPA 2027 developments and procurement timing

The Class 8 outlook is more constructive, but purchasing is likely to remain selective and closely connected to replacement exposure and financial capacity.

Medium Duty

Medium-duty demand remains more cautious than Class 8. Many of the economic drivers supporting Classes 5–7—including consumer confidence, housing, small-business investment, and other interest-rate-sensitive activity—remain uneven.

Recent order improvement is encouraging, but it does not yet establish broad-based acceleration. Demand also varies meaningfully by application. Vocational and service-oriented equipment may continue to receive support from infrastructure, utility, energy, construction, and data-center-related investment. Consumer- and housing-sensitive applications remain more exposed to financing pressure and weaker confidence.

For 2027, the medium-duty truck forecast depends on whether improved order intake converts into sustained retail activity across vocational, regional, leasing, delivery, and small-business-sensitive segments. The segment is less directly connected to long-haul freight-rate improvement than Class 8, making application-level demand particularly important.

Dealers, leasing companies, manufacturers, suppliers, and lenders should plan for selective improvement rather than assuming a broad acceleration. Key indicators include retail follow-through, body-builder throughput, customer delivery schedules, financing conditions, and demand within individual applications.

Trailers

The trailer market forecast for 2027 is becoming more constructive, but the recovery remains less established than the Class 8 upturn. Firmer truckload rates and tighter capacity are supporting replacement discussions, while improving order activity suggests fleet confidence is beginning to strengthen.

Purchasing remains primarily replacement-focused rather than expansion-driven. Backlog quality, cancellations, financing conditions, and segment-level demand therefore require continued attention before the trailer market can be characterized as a broad upcycle.

Conditions also differ by trailer type. Dry van demand is receiving support from tighter truckload capacity and higher rates. Reefer replacement needs remain relevant because of specialized-capacity requirements and fleet age. Flatbed and vocational trailer demand continues to benefit from construction, infrastructure, utility, energy, and project-related activity.

For fleets, trailer manufacturers, suppliers, dealers, leasing companies, and lenders, the most useful 2027 signals will be:

- Backlog rebuilding and backlog quality

- Cancellation behavior

- Order-to-build conversion

- Fleet utilization and profitability

- Replacement timing by trailer category

- Financing availability

- Whether stronger freight conditions produce sustained commitments

The market is improving at the margin, but stronger backlog coverage and continued order follow-through are still needed to confirm broader strength.

Regulatory and Cost Environment

Regulatory timing and compliance enforcement remain central to the Trucking Industry Forecast 2027. EPA 2027 may influence replacement schedules, buyer behavior, equipment-cost expectations, production planning, and procurement windows.

Fleets are evaluating the cost and availability of future equipment alongside the economics of keeping older assets in service. Manufacturers and suppliers must prepare for potential prebuy demand without assuming that customer interest will convert uniformly into firm orders and completed deliveries.

Other policy and enforcement developments are already affecting available capacity. Driver-qualification requirements, FMCSA activity, ELD-related enforcement, driver-school constraints, and other compliance measures are making it more difficult for marginal capacity to remain in or return to the market.

These developments matter for 2027 because they may affect:

- Carrier availability and pricing power

- Fleet utilization and driver productivity

- Routing-guide reliability

- Procurement and bid timing

- Carrier profitability

- Equipment replacement and financing demand

Cost pressure remains a significant constraint. Insurance, financing, labor, maintenance, and equipment prices continue to shape fleet investment strategies. For many fleets, 2027 planning will emphasize replacement discipline, operational efficiency, liquidity, uptime, and total cost of ownership rather than broad capacity expansion.

Outlook for 2027

The Trucking Industry Forecast 2027 points to a market that may enter the year on firmer footing than the prior cycle, but with disciplined fleet behavior still intact. The current upturn is being led primarily by supply tightening rather than a broad freight-demand surge. That distinction matters for budgeting, procurement, equipment replacement, production planning, lending, leasing, and investment strategy.

Class 8 is receiving the clearest support from improving freight economics, constrained capacity, replacement needs, and regulatory planning. Medium-duty demand is improving more selectively and remains dependent on application-level follow-through. Trailer conditions are becoming more constructive, but broader strength will require sustained replacement confidence and backlog rebuilding.

For transportation and commercial vehicle decision-makers, 2027 planning should focus on:

- Freight-rate durability and contract-reset timing

- Driver availability and the persistence of capacity contraction

- Carrier margin conversion and cash flow

- EPA 2027 timing and potential prebuy activity

- Equipment replacement and procurement windows

- Financing sensitivity and operating-cost recovery

- Used-truck values and residual risk

- Order conversion, cancellations, and backlog quality

- Segment- and application-specific demand

ACT Research helps customers evaluate these connected market-cycle signals through forward-looking Freight Intelligence, Commercial Vehicle Intelligence, and Equipment Market Intelligence. Connecting freight demand, rates, capacity, equipment production, replacement timing, and used values provides a stronger basis for 2027 planning than relying on any single indicator.

Stay Ahead with Smarter Freight Insights

Success in trucking and freight comes from knowing what’s next—not just what’s now. At ACT Research, we deliver forward-looking market intelligence that helps you anticipate shifts, prepare for cycles, and stay strategically positioned. As your trusted transportation intelligence partner, we give you the tools to act with confidence—so you can optimize operations, reduce risk, and drive stronger profitability.