2026 Class 8 Truck Market

June 2026

Updated June 29, 2026

The Class 8 Tractor Sales Forecast 2026 continues to improve as freight conditions tighten, tractor demand strengthens, and fleet sentiment becomes more constructive. The market is not yet in a broad expansion cycle, but current signals show a clearer transition away from the prolonged downcycle that shaped 2024 and 2025.

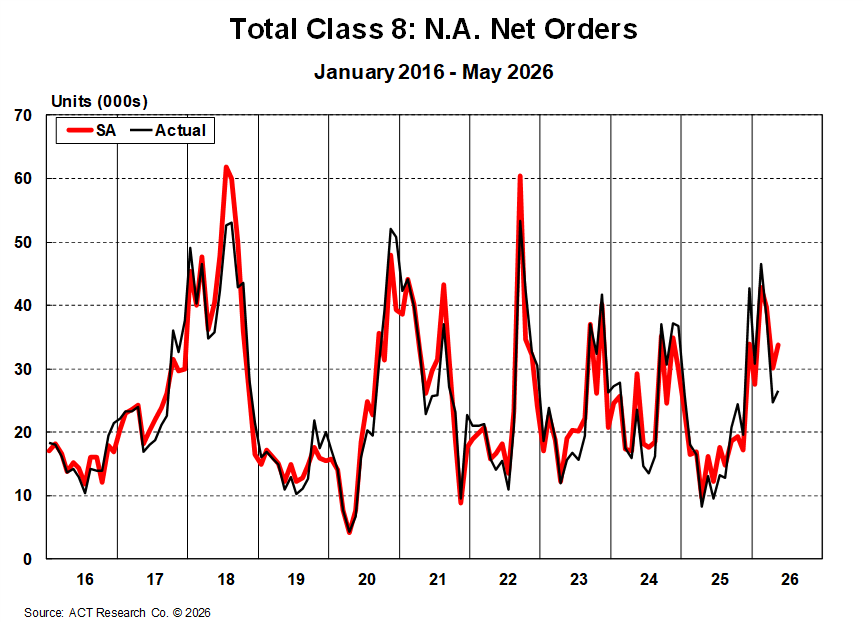

ACT’s June reports point to a supply-driven recovery that has gained momentum. Truckload capacity has tightened, spot rates have strengthened sharply, and contract rates are accelerating. Class 8 order activity strengthened in May, with North American Class 8 orders up sharply year-over-year and higher sequentially on a seasonally adjusted basis. Tractor demand led the improvement, supported by better freight rates, tighter capacity, and EPA 2027 planning.

Infrastructure and Construction Support

Vocational Class 8 demand remains supported by longer-cycle infrastructure, utility, energy, and data-center-related investment. ACT’s June Commercial Vehicle Outlook notes that large technology investments in data centers, utilities, and grid-related work continue to support vocational truck demand.

For 2026 planning, the key point is that vocational demand remains resilient, while tractor demand is now benefiting more directly from the freight-rate recovery. Infrastructure-aligned activity and AI-related data center investment may continue to support medium-term visibility, but broader goods-producing demand remains uneven.

Production and Backlogs

Class 8 production remains disciplined, but order and backlog signals are more constructive than they were through much of the prior downcycle. ACT’s latest Classes 5–8 data shows Class 8 backlogs increased to a 36-month high in May, while build plans improved for Q2 through Q4.

That matters for fleets, buyers, dealers, lenders, and suppliers because the market is gaining forward visibility without showing signs of uncontrolled expansion. Replacement needs, rate improvement, and regulatory timing are supporting demand, while financing costs and operating expenses continue to keep fleet buying behavior disciplined.

Regulatory Shifts

Regulatory timing remains one of the most important planning variables in the 2026 Class 8 truck market. EPA 2027 continues to influence replacement timing, procurement planning, and expectations for higher future equipment costs. Stronger freight conditions are also making it easier for some fleets to evaluate replacement decisions ahead of regulatory change.

Driver-related policy changes are also affecting the market. ACT’s June Freight Forecast points to falling driver availability, nondomiciled CDL rules, FMCSA-related enforcement, fraudulent ELD removals, driver school closures, and other supply-side constraints as contributors to tighter capacity. These developments are supporting freight-rate momentum and improving the economics behind replacement decisions.

Capacity Rebalancing

The Class 8 sector continues to rebalance as capacity tightens and freight rates improve. ACT’s June Freight Forecast notes that the truckload market has entered a period of rising rates and tight capacity, with driver availability falling sharply. Contract rates also accelerated in May, confirming that pricing improvement is moving beyond spot-market disruption.

Used truck signals are also becoming more constructive. ACT’s June Used Trucks report shows May same-dealer used Class 8 retail sales improved year-over-year, while average retail pricing was also higher year-over-year. For fleets and lenders, stronger used truck values may help improve residual-value visibility and support replacement-cycle confidence.

Moderate Growth in Orders

Class 8 order activity is no longer at trough levels, but the market remains disciplined. May orders strengthened materially, with tractor orders leading the gain as freight-rate conditions improved and fleets looked ahead to EPA 2027 timing.

For commercial vehicle decision-makers, this points to a measured recovery rather than a broad-based surge. Fleet replacement demand is improving, but purchase decisions remain sensitive to financing conditions, operating costs, future equipment pricing, and confidence in rate durability.

Economic Tailwinds and Risks

The 2026 Class 8 truck market is benefiting from improving freight economics, infrastructure-related activity, and tightening capacity. At the same time, insurance, financing, maintenance, equipment, and labor costs continue to affect carrier profitability and equipment-purchase timing.

ACT’s June Freight Forecast shows that spot market strength is now moving into contract pricing, with aggregate DAT contract rates nearly 10% above year-ago levels in May. If rate improvement remains durable, it may support stronger fleet confidence and replacement activity through the balance of 2026.

The practical takeaway: the Class 8 tractor market is on firmer footing than earlier in the cycle, but demand is still being shaped by replacement discipline, regulatory timing, and supply-driven rate recovery rather than broad expansion. Fleets, buyers, dealers, lenders, leasing companies, and investors should continue monitoring freight-rate sustainability, driver availability, EPA 2027 timing, used truck values, and financing conditions as the 2026 truck market develops.

Want more data?

ACT’s commercial vehicle forecast delivers the most reliable, forward-looking insight into where Class 8 truck sales are headed—helping you anticipate shifts, plan with confidence, and stay ahead of the market.