According to this month’s issue of ACT Research’s State of the Industry: U.S. Trailers report, with equipment order intake improving, freight rates increasing, policy impacts becoming clearer, and despite concerns remaining, optimism is on the rise.

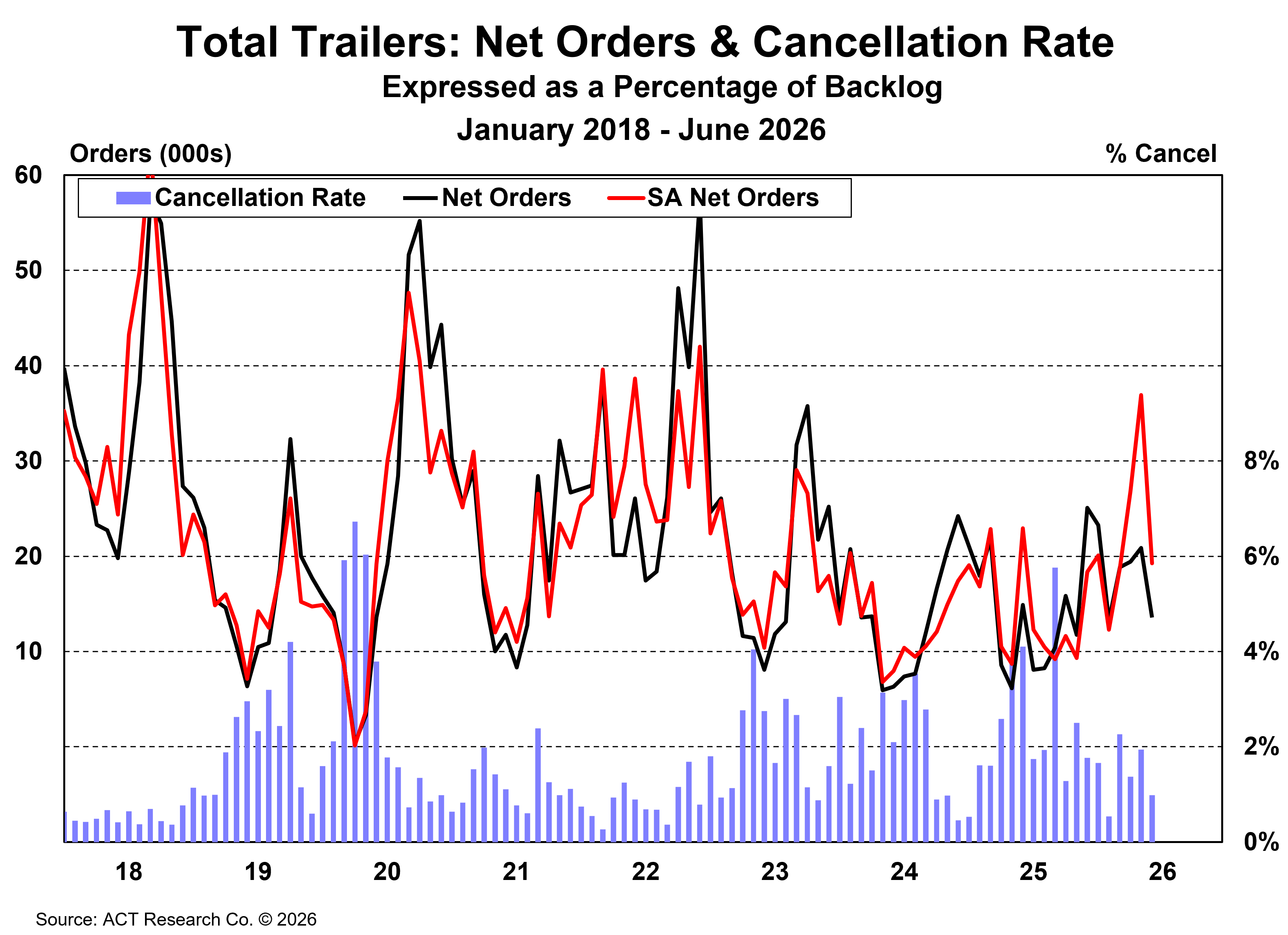

“After delivering counter to cyclical expectations results the past three months, net order intake in June slowed in seasonal fashion. Net US trailer orders in June were 13,500 units, down about 7,300 units from May, a 35% month-to-month decrease. Compared to June 2025, this year’s intake was 1,300 units lower, nearly a 9% decrease,” said Jennifer McNealy, Director–CV Market Research & Publications at ACT Research. “June’s cancellation rate of 1.0%, as a percentage of backlog, dropped from ‘elevated’ territory, and now sits at the top of the target range. Still, it is an improvement from May’s 1.9% cancellation rate. Like last month, high cancellations were reported in most segments, meaning the situation was broad-based.”

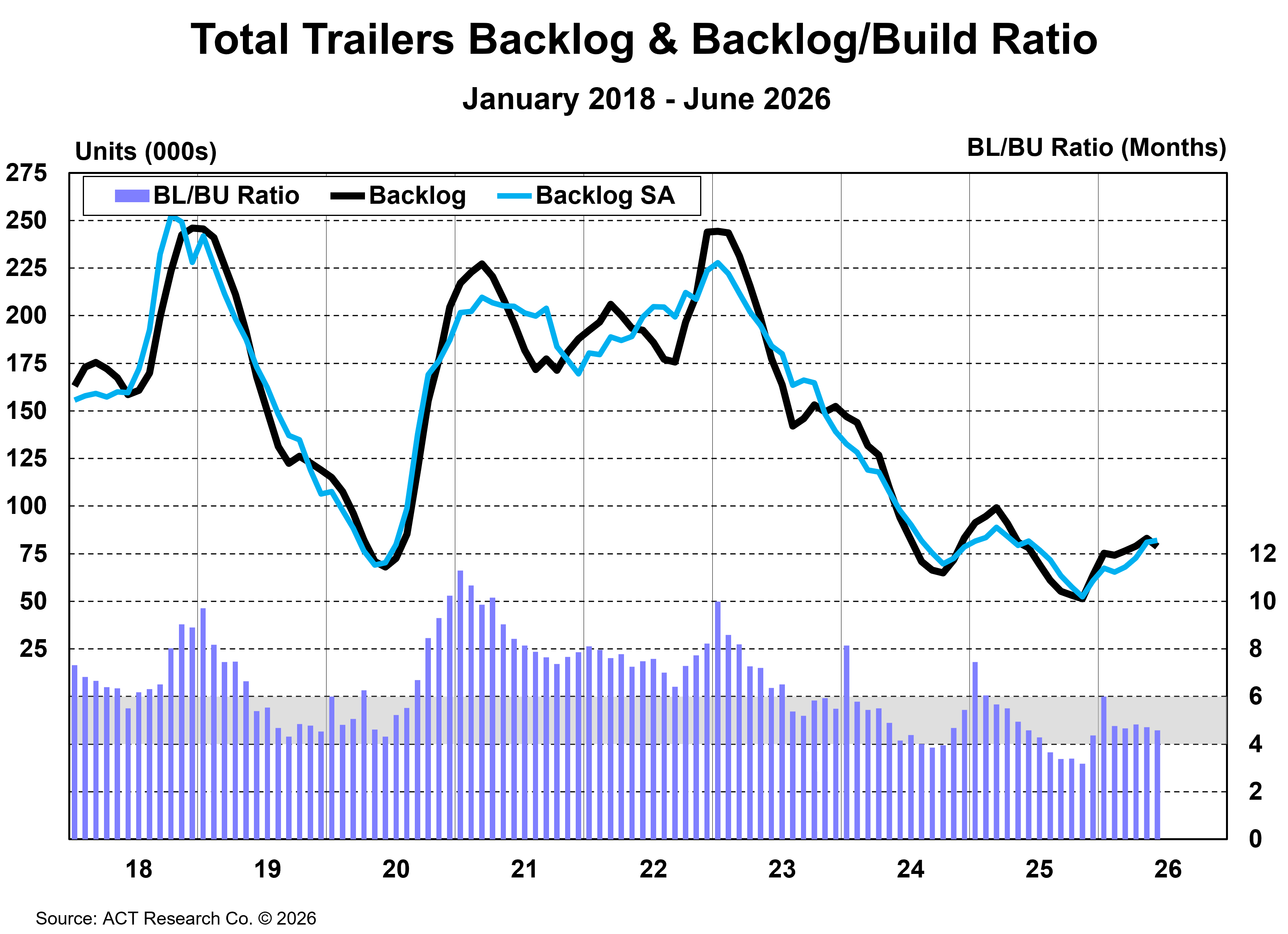

“Net orders have now outpaced build for four of the six months in 2026. June was one of the four, as about 4.5k more trailers were built than ordered, shrinking the backlog by 5% m/m, which doesn’t help the already anemic backlogs,” McNealy concluded.

State of the Industry: U.S. Trailers Report Overview

ACT Research’s State of the Industry: U.S. Trailers report provides a monthly review of the current US trailer market statistics, as well as trailer OEM build plans and market indicators divided by all major trailer types, including backlogs, build, inventory, new orders, cancellations, net orders, and factory shipments. It is accompanied by a database that gives historical information from 1996 to the present, as well as a ready-to-use graph packet, to allow organizations in the trailer production supply chain, and those following the investment value of trailers, trailer OEMs, and suppliers to better understand the market.

ACT Research Overview

ACT Research is recognized as the leading publisher of commercial vehicle truck, trailer, and bus industry data, market analysis, and forecasts for the North America and China markets. ACT’s analytical services are used by all major North American truck and trailer manufacturers and their suppliers, as well as banking and investment companies. ACT Research is a contributor to the Blue Chip Economic Indicators and a member of the Wall Street Journal Economic Forecast Panel. ACT Research executives have received peer recognition, including election to the Board of Directors of the National Association for Business Economics, appointment as Consulting Economist to the National Private Truck Council, and the Lawrence R. Klein Award for Blue Chip Economic Indicators’ Most Accurate Economic Forecast over a four-year period. ACT Research senior staff members have earned accolades including Chicago Federal Reserve Automotive Outlook Symposium Best Overall Forecast, Wall Street Journal Top Economic Outlook, and USA Today Top 10 Economic Forecasters. More information can be found at www.actresearch.net.

Additional Resources

Preliminary net trailer orders in June were 13,500 units. June orders were down about 7,300 units from May, a 35% month-to-month decrease, and 1,300 units lower than June 2025, down nearly 9%. Seasonal adjustment (SA) at this point in the annual order cycle takes the month’s volume to 19,200 units. Final June trailer industry data will be available later this month. This preliminary order estimate is typically within ±5% of the final order tally.

“After several months with net orders behaving counter to historical patterns, the seasonal slowing of orders arrived with the June data,” said Jennifer McNealy, Director CV Market Research & Publications at ACT Research. She continued, “Typically, March starts the seasonal slowing of orders, as fleets have made their decisions for current-year needs and OEMs start to build down the backlog. June traditionally marks the third weakest order month of the annual order cycle. That said, this year’s cycle has been anything but ordinary: the order upticks that should have started in September or October of last year didn’t actually begin until December. The atypical strength in orders in April and May reflects improving trucking fundamentals, buttressed by rising freight rates.”

McNealy concluded, “Regardless of the timing, the order upticks certainly were welcome, but were premature in terms of 2027 order timing and the opening by OEMs of next year’s calendars. Additionally, caution remains a strategy for some trailer purchasers. Rates are rising now, but the past few years have been hard for carriers, and now the challenges of strong pent-up demand and the risks of higher maintenance costs and downtime to repair rather than purchase new equipment remain as counter-weights to their decision-making process.”

- Cancellation Rate as a % of Backlog: 1.0%

- Backlogs: -5% m/m

Click here to learn more information about ACT's Mexican Trailer Market report.

ACT Research is featured regularly by major news outlets for our work covering Class 8 truck orders, sales, forecasting, used truck sales, freight rates, trailer sales, and much more. Get more trends, HERE.

Save time with ACT Research’s media kit. Access ACT Research’s analyst bio, logos, press releases, video library, and more at your convenience. Our analysts are committed to delivering the most accurate data and forecasts. Looking for a speaker? Each analyst is available to speak at your conference or event. Access Media Kit Here.