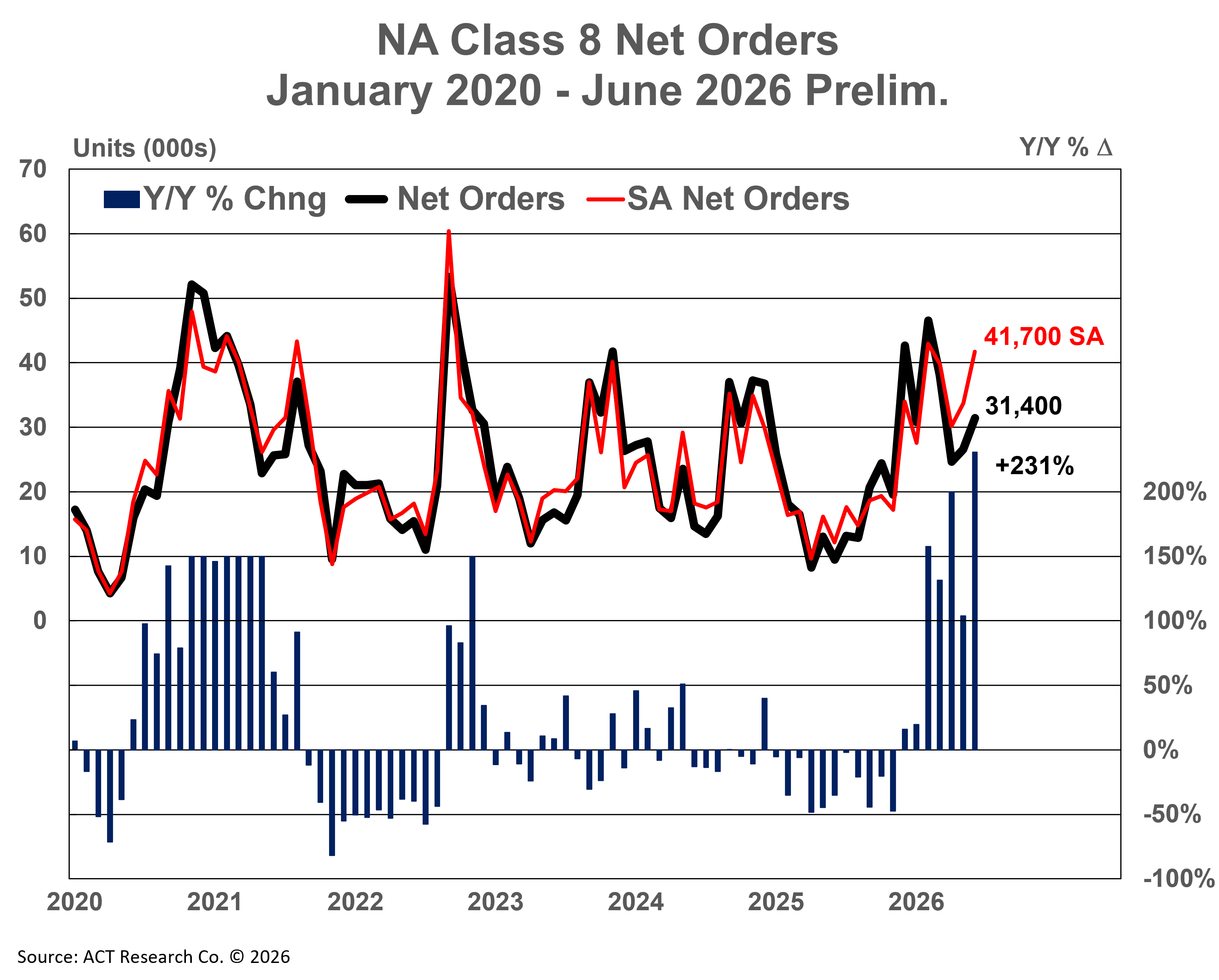

June preliminary North America Class 8 net orders of 31.4k units increased 231% y/y. Complete industry data for June, including final order numbers, will be published by ACT Research in mid-July.

“Strong orders this month, adding to an already full Class 8 backlog, suggest either higher than expected industry builds into year-end or orders increasingly spilling into 1H’2027. Underpinning the 7-month run of strong Class 8 order activity has been the ongoing, supply lead and demand supported recovery in the trucking industry. As we say, truckers only buy trucks when they make money. Underscoring the rapid change in carrier fortunes, freight rates continue to soar,” shared Carter Vieth, Research Analyst at ACT Research.

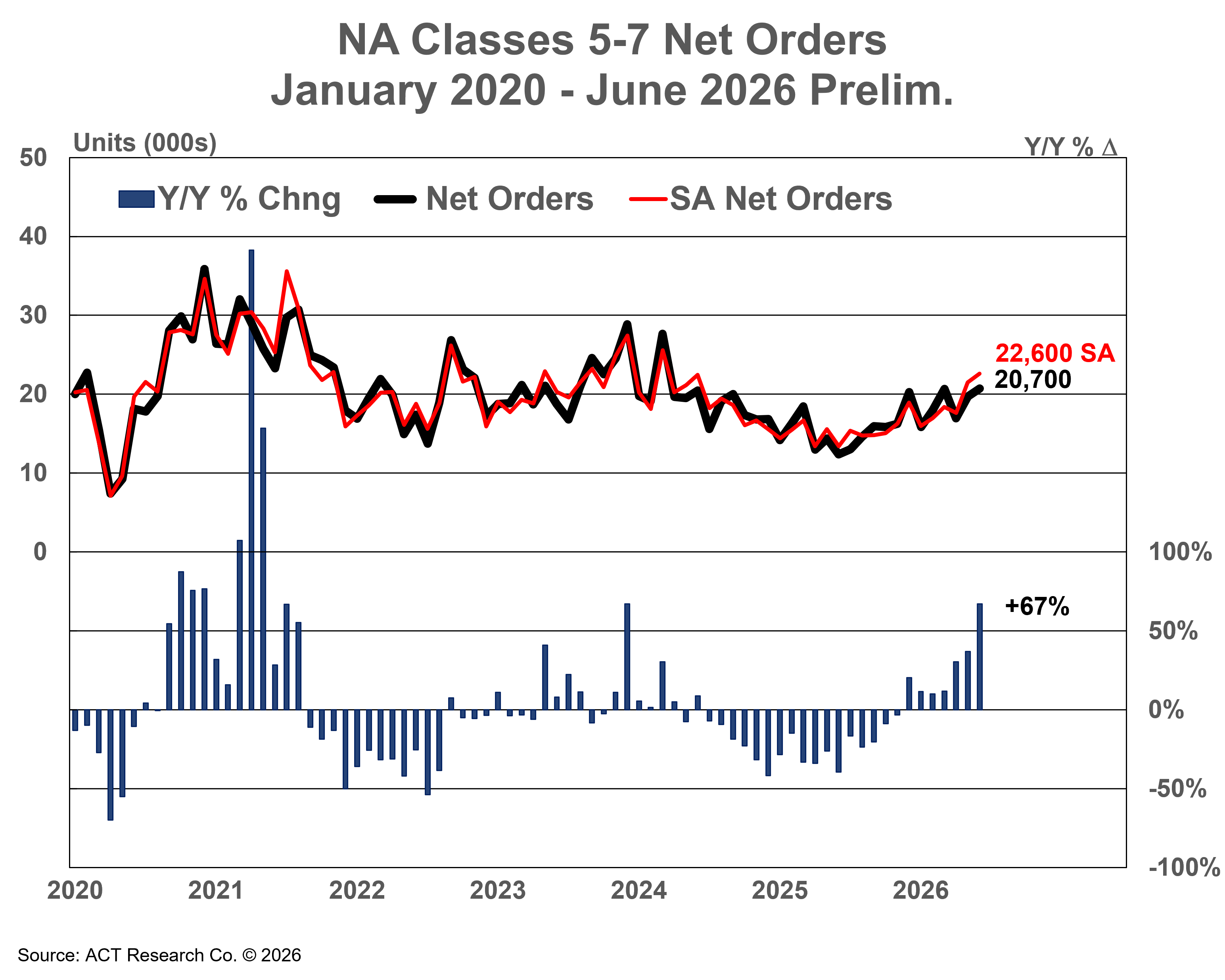

Regarding medium duty, he added, “Preliminary Classes 5-7 orders rose 67% y/y to 20,700 units in June. The US’s ongoing economic resilience is certainly aiding medium-duty demand, but given near record low consumer sentiment and the very real sticker shock hitting small-to-medium fleets, this month’s medium-duty orders appear to be driven largely by dealer inventory stocking ahead of 2027.”

State of the Industry: NA Classes 5-8 Report Overview

ACT’s State of the Industry: NA Classes 5-8 report provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America. It differentiates market indicators by Class 5, Classes 6-7 chassis and Class 8 trucks and tractors, detailing measures such as backlog, build, inventory, new orders, cancellations, net orders, and retail sales. Additionally, Class 5 and Classes 6-7 are segmented by trucks, buses, RVs, and step van configurations, while Class 8 is segmented by trucks and tractors with and without sleeper cabs. This report includes a six-month industry build plan, backlog timing analysis, historical data from 1996 to the present in spreadsheet format, and a ready-to-use graph package. A first-look at preliminary net orders is also published in conjunction with this report.

ACT Research Overview

ACT Research is recognized as the leading publisher of commercial vehicle truck, trailer, and bus industry data, market analysis and forecasts for the North America and China markets. ACT’s analytical services are used by all major North American truck and trailer manufacturers and their suppliers, as well as banking and investment companies. ACT Research is a contributor to the Blue Chip Economic Indicators and a member of the Wall Street Journal Economic Forecast Panel. ACT Research executives have received peer recognition, including election to the Board of Directors of the National Association for Business Economics, appointment as Consulting Economist to the National Private Truck Council, and the Lawrence R. Klein Award for Blue Chip Economic Indicators’ Most Accurate Economic Forecast over a four-year period. ACT Research senior staff members have earned accolades including Chicago Federal Reserve Automotive Outlook Symposium Best Overall Forecast, Wall Street Journal Top Economic Outlook, and USA Today Top 10 Economic Forecasters. More information can be found at www.actresearch.net.

Additional Resources

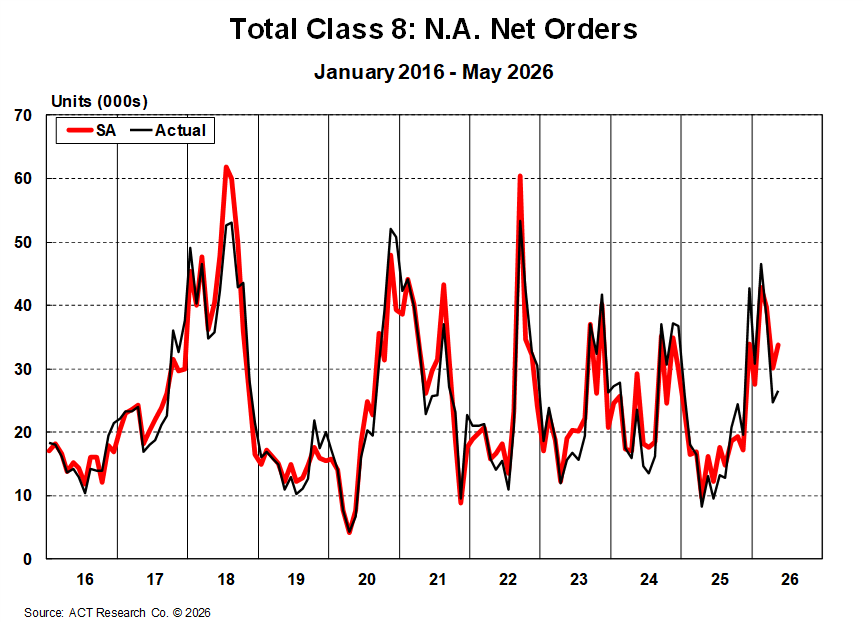

Final North American Class 8 net orders totaled 26,576 units in May, up 104% y/y and 12% m/m on a seasonally adjusted basis, as published in ACT Research’s latest State of the Industry: NA Classes 5-8 report.

“Demand for new equipment remains robust, driven by the sustained and supply-side-led run up in freight rates and looming cost increases associated with EPA’27 regulations come January 1,” according to Carter Vieth, Research Analyst at ACT Research. “With freight conditions quickly improving, tractor orders rose 126% y/y, totaling 19,098 units in May. Vocational Class 8 orders totaled 7,478 units, increasing 63% y/y. With AI hyperscalers spending ~$15–$20 billion per week on infrastructure, vocational demand continues to benefit from tech tailwinds.”

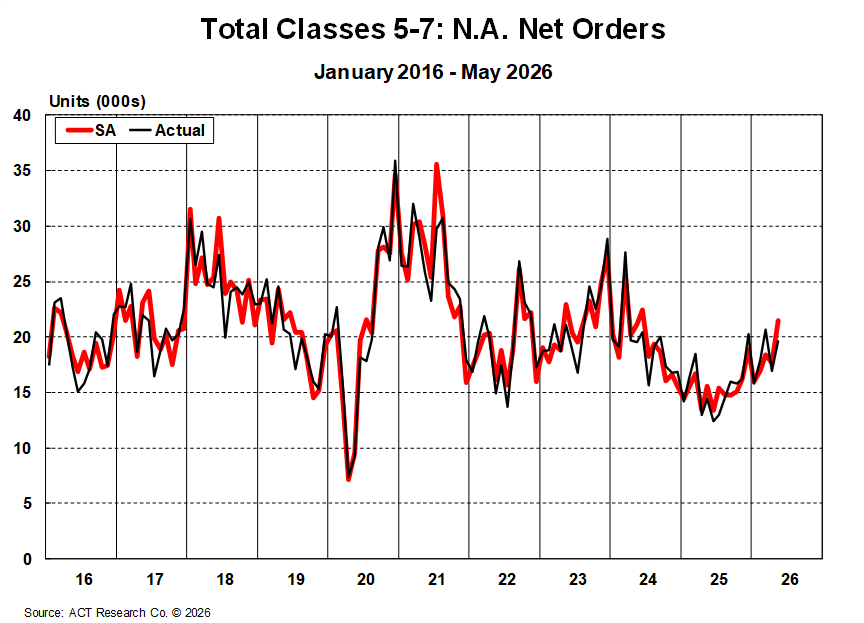

Regarding medium duty, Vieth added, “Total Classes 5-7 orders rose 37% y/y to 19,725 units, perhaps reflecting continued US economic resilience, particularly among consumers, despite record, or near record, low confidence levels. Orders this month suggest some level of dealer inventory stocking ahead of 2027, especially as recent customer anecdotes indicate lack of large order appetite for medium duty.”

Class 8:

Net Orders: 26,576

Classes 5-7:

Net Orders: 19,725

Click here to learn more information about ACT's State of the Industry: NA Classes 5-8 Vehicles data.

ACT Research is featured regularly by major news outlets for our work covering Class 8 truck orders, sales, forecasting, used truck sales, freight rates, trailer sales, and much more. Get more trends, HERE.

Save time with ACT Research’s media kit. Access ACT Research’s analyst bio, logos, press releases, video library, and more at your convenience. Our analysts are committed to delivering the most accurate data and forecasts. Looking for a speaker? Each analyst is available to speak at your conference or event. Access Media Kit Here.