Dry Van Rates

Dry Van Freight Rates: Spot & Contract Market Trends - June 2026

ACT Research provides data-driven insight into dry van spot and contract rate movements, helping industry leaders understand pricing trends and freight market conditions.

Dry Van Truckload (TL) Sector

June 2026 Update

June 26, 2026

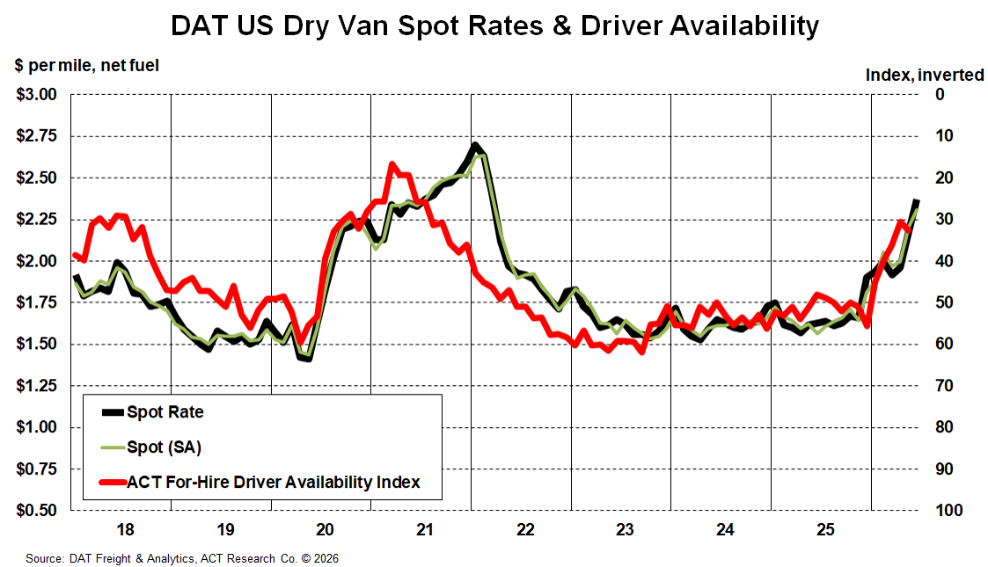

As of June 2026, dry van rates continue to strengthen as the truckload market moves further into a supply-driven recovery. Freight demand is improving in pockets, but the larger market shift is coming from constrained capacity, lower driver availability, regulatory enforcement, and limited fleet expansion. ACT’s June Freight Forecast notes that the market has entered a period of rising rates and tight capacity, with driver availability falling sharply.

The dry van market is no longer reacting only to Roadcheck or short-term disruption. Spot rates remain materially higher year-over-year, and contract rates are accelerating as tighter capacity works through bid cycles. Shipper leverage has narrowed, while carriers are seeing improved pricing power, even as insurance, labor, financing, equipment, and other operating costs continue to pressure margins.

Spot Rates

Dry van spot rates strengthened again in May, supported by constrained capacity, stronger spot demand, and tighter load-to-truck conditions around Roadcheck. ACT’s June Freight Forecast reported that DAT U.S. dry van truckload spot rates, net fuel, rose sharply year-over-year in May, accelerating from April.

Some seasonal moderation remains possible, but the broader rate floor appears higher than it was during the prior downturn. Fewer available drivers, regulatory pressure, and limited replacement activity are making it harder for capacity to respond quickly to better rates.

Contract Rates

Dry van contract rates are now responding more clearly to sustained spot-market strength. Aggregate DAT contract rates rose again in May and were nearly 10% above year-ago levels, signaling that the pricing reset is moving beyond spot volatility and into broader bid activity.

For shippers, this means bid activity may become less favorable as the year progresses. For carriers, stronger contract pricing should support revenue quality, though profitability remains dependent on managing elevated operating costs.

Capacity Conditions

Capacity remains the primary driver of the dry van rate recovery. Driver availability has tightened, regulatory and enforcement pressure has increased, and below-replacement tractor sales in the prior downcycle limited the pace of fleet expansion. ACT’s June commercial vehicle commentary also points to new supply lows as nondomiciled CDL rules, the new USDOT registration system, fraudulent ELD removals, and driver school closures continue to remove or limit capacity.

Private fleet contraction is also shifting more freight back toward the for-hire market. That dynamic, combined with disciplined fleet expansion and stronger spot demand, is reinforcing a tighter dry van environment even without a broad freight demand surge.

Summary

The dry van TL market is firmer entering June 2026, with pricing strength increasingly tied to structural capacity tightening rather than temporary disruption. Spot rates remain elevated, contract rates are improving, and capacity conditions continue to favor carriers more than they did during the prior downturn.

Demand remains uneven, and cost pressure is still limiting fleet expansion. Even so, the dry van market appears to be moving further into recovery. Shippers, carriers, brokers, fleets, and investors should continue monitoring load-to-truck trends, contract bid activity, driver availability, regulatory enforcement, and whether higher rates translate into healthier carrier profitability.

As of June 2026, dry van rates remain firmly above prior-cycle lows, with pricing support increasingly tied to structural capacity tightening rather than short-term disruption. Roadcheck added near-term pressure in May, but the broader trend is being driven by constrained driver availability, regulatory enforcement, and limited fleet expansion. Freight demand remains uneven, but load-to-truck conditions have tightened enough to support higher rate floors and shift more leverage back toward carriers.

Contract rates are now responding more clearly as spot-market strength works through bid cycles. ACT’s June Freight Forecast shows aggregate truckload contract rates accelerating year-over-year in May, signaling that the recovery is moving beyond spot-market volatility and into broader pricing resets. While seasonal volatility is still possible, the dry van market continues to move toward balance, with durable rate momentum increasingly supported by capacity contraction, compliance pressure, and cost discipline rather than a broad demand-led surge.

Tim Denoyer

VP & Sr. Analyst

Resources

Whether you’re new to our company or are already a subscriber, we encourage you to take advantage of all our resources.