Class 8 Truck Orders

March 2026 Class 8 Truck Orders & Industry Outlook

ACT Research delivers proprietary, forward-looking analysis of Class 8 truck orders to help industry leaders plan capacity and capital investments with confidence.

Class 8 Truck Orders

March 27, 2026 Update

As of March 2026, the Class 8 truck market is entering a more defined inflection point, with the recovery increasingly driven by supply-side tightening rather than a meaningful acceleration in freight demand. Spot market conditions remain firm, with aggregate spot rates running approximately 20% higher year-over-year, supported by a sharp contraction in available capacity and rising fuel-driven cost pressures. Contract rates have also begun to accelerate, signaling the early stages of a broader pricing reset across the market.

Carrier profitability remains constrained but is stabilizing, as improved rate conditions are partially offset by a rapid increase in diesel prices and broader operating costs. Public carriers continue to operate under margin pressure, though fuel surcharges and stronger contract pricing are beginning to improve revenue quality. Private fleets remain disciplined, but ongoing contraction in private capacity is increasingly shifting freight back into the for-hire market, accelerating the rebalancing process.

While overall freight demand remains below peak-cycle levels, the supply-demand balance is tightening more quickly than anticipated. Driver availability has declined meaningfully, approaching levels historically associated with the beginning of prior rate cycles, while regulatory changes tied to nondomiciled drivers are expected to further constrain capacity over the next several quarters. Combined with prior production cuts and limited fleet expansion, these dynamics are driving a faster transition toward equilibrium as 2026 progresses into March.

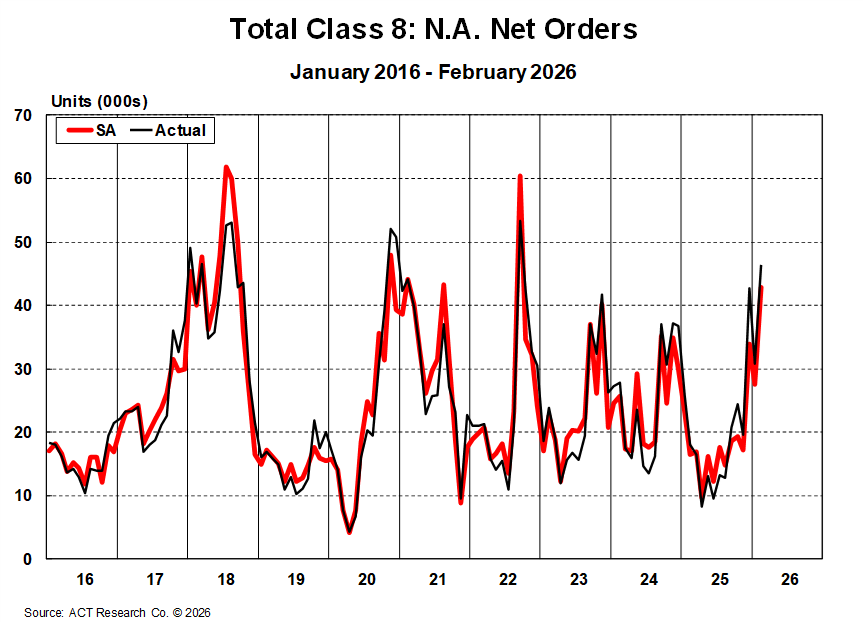

Following strong order activity through December, January, and February, momentum entering March remains well above replacement demand levels and continues to reflect improving carrier sentiment. February orders surged to over 46,000 units, representing a significant year-over-year increase and marking one of the strongest order months in the current cycle.

ACT Research Class 8 Net Orders - March 2026

The sustained strength in order intake over the past three months confirms that activity is no longer limited to year-end catch-up dynamics. Instead, improving rate conditions, tightening capacity, and regulatory timing are now translating into more durable forward demand. Seasonally adjusted order rates remain at their highest levels in over a year, reinforcing the view that the market is transitioning off the bottom.

Backlog levels expanded further in February, reaching multi-year highs, while the backlog-to-build ratio remains elevated as OEMs continue to manage production cautiously. Build plans for the first half of 2026 have improved modestly but remain disciplined, reflecting a continued focus on aligning production with confirmed demand rather than speculative growth.

Production discipline remains a defining theme. OEMs are maintaining controlled output levels despite stronger orders, preserving backlog visibility and supporting pricing stability. While build rates have improved from weather-disrupted levels earlier in the year, overall production continues to reflect a measured approach to recovery.

Inventory conditions remain mixed. Tractor inventories are largely normalized following production cuts throughout 2025, while vocational inventories remain elevated relative to historical norms. Retail sales continue to lag year-over-year, highlighting that while the rate environment is improving, fleet capital deployment remains selective and tied closely to profitability expectations.

The §232 heavy-vehicle tariffs tied to foreign content value remain embedded in OEM pricing, while broader trade policy developments, including recent tariff rollbacks, are expected to provide a modest tailwind to freight demand later in 2026. At the same time, rising input costs, including fuel, insurance, and equipment, continue to pressure total cost of ownership and reinforce disciplined purchasing behavior across fleets.

Class 8 Truck Orders Snapshot

Entering March 2026, Class 8 order activity reflects a market that has moved beyond the bottoming phase and is now in the early stages of a supply-driven recovery. The strength observed since December has been reinforced by tightening capacity, improving pricing, and increasing regulatory clarity.

OEMs continue to carefully manage daily build rates, ensuring alignment with backlog while avoiding premature capacity expansion. Dealer feedback suggests that retail demand remains measured outside of large fleet commitments and regulatory-driven purchases, reinforcing that the recovery remains uneven across customer segments.

Used Class 8 market dynamics remain mixed. Retail volumes improved sequentially in February but continue to trail year-ago levels, while pricing has stabilized modestly on a year-over-year basis. Elevated fuel prices and ongoing cost pressures are expected to create near-term volatility in secondary markets, particularly for smaller operators.

Freight fundamentals continue to improve, though primarily as a result of constrained supply rather than a surge in demand. Spot market strength, rising load-to-truck ratios, and declining driver availability all point to a tightening capacity environment. However, near-term volatility remains likely as seasonal factors normalize and fuel costs continue to fluctuate.

Absent a sustained improvement in carrier profitability, some volatility should be expected through the first half of 2026. However, the underlying structural setup—tightening capacity, regulatory pressure, disciplined production, and deferred replacement demand—supports a more constructive outlook. A more durable and balanced recovery is increasingly likely to take shape in the second half of 2026, with stronger upside potential extending into 2027 as rate strength, regulatory dynamics, and fleet investment cycles further align.

With tractor orders surging through February and maintaining strong year-over-year growth, orderboards are rebuilding from historically depressed levels, even as OEMs continue to manage production conservatively. The Class 8 market’s challenge has shifted decisively—from backlog erosion and weak demand to a supply-driven early-cycle recovery defined by tightening capacity, rising rates, and still-fragile carrier profitability. Regulatory visibility around EPA 2027 continues to support planning, while new driver-related policy changes are expected to further constrain capacity, and tariff-driven cost inflation alongside a sharp increase in diesel prices are adding pressure to total cost of ownership. While vocational demand remains resilient and improving rate conditions are lifting sentiment, retail activity is still measured, leaving fleets focused on disciplined replacement and regulatory positioning rather than broad-based expansion.

Kenny Vieth

President & Senior Analyst

Resources

Whether you’re new to our company or already a subscriber, we encourage you to take advantage of all our resources.